The Influence of Job Rotation, Competency, and Audit Tenure on The Quality of Audit Results Through the Independence of the Auditors of PT Difaya Terampil Mandiri

Submission to VIJ 2024-03-25

Keywords

- Job Rotation, Competency, Audit Tenure, Auditor Independence, Quality of Audit Results

Copyright (c) 2024 Deby Cahya Purnama, Ismail Razak, Partogi S Samosir

This work is licensed under a Creative Commons Attribution 4.0 International License.

Abstract

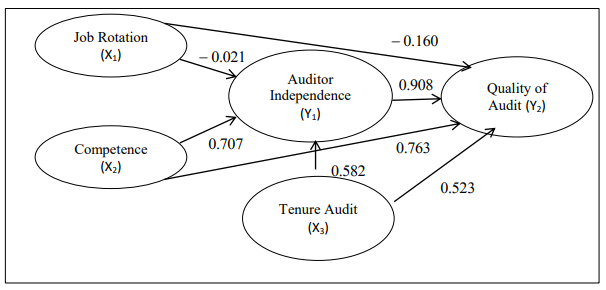

This research aims to analyze the influence of work rotation, competency, and audit tenure on the quality of audit results through auditor independence. The quality of the results is an important result for stakeholders and companies that have carried out inspections. This research method involves quantitative analysis to understand the basic concept of audit result quality. Furthermore, this research will conduct a case study analysis of work rotation, competency, audit tenure, auditor independence, and the quality of audit results. The data obtained will be analyzed using path analysis. It is hoped that the research results will provide an in-depth understanding of how work rotation, competency, and audit tenure influence the quality of audit results through auditor independence. These findings can be a basis for recommending more effective implementation strategies in realizing good-quality audit results. The findings in this research are that work rotation does not have a significant effect on auditor independence and also the quality of audit results, competency, and audit tenure have a significant effect on auditor independence and the quality of audit results, auditor independence as a mediating variable can only mediate audit tenure on the quality of audit results.

References

- Andi Ibrahim Yunus, Roy Setiawan, Rusydi Fauzan, Kurnia Widyaningrum, Kadek Wiwin Dwi Wismayanti, Desi Kristanti, Selvi Yona Tamara, Purna Irawan, Sundari, Eni Erwantiningsih, Solehudin, Sabil, Monica Feronica Bormasa, Tini Elyn Herlina, Septia Dwi Cahyani, Putu Eka Purnamaningsih, Iwan Henri Kusnadi, & Jasman. (2023). Manajemen Sumber Daya Manusia (Teori) (D. Purnama Sari, Ed.; 1st ed., Vol. 1). PT Global Eksekutif Teknologi.

- Arens, A. A., Randal, J. E., & Beasley, M. (2011). Audit dan Jasa Assurance: Pendekatan Terpadu (Penerjemah Herman Wibowo). Salemba Empat.

- Arfiangga, O., & Kristianto, D. (2014). Pengaruh Kompetensi auditor, Audit Fee dan Good Corporate Governance Terhadap Indepedensi Auditor. Jurnal Akuntansi Dan Sistem Teknologi Informasi, Issn 1693-7635, 10.

- Asmoro, Prabowo Hadi, Saraswati, Erwin, Baridwan, & Zaki. (2022). The effect of auditor rotation, fee, tenure, and professional skepticism on audit quality. International Journal of Research in Business and Social Science, 11, 221–231.

- Chesoli, J. W. (2020). The role of auditor independence in the relationship between mandatory auditor rotation and audit quality: A critical literature review. IJRDO - Journal of Business Management, 5(12), 20-69., 5.

- Dessler, & Gary. (2017). Human Resource Management. Pearson Education Limited, Inc.

- Duryadi. (2021). Buku Ajar Metode Penelitian Ilmiah, Metode Penelitian Empiris Model Path Analysis dan Analisis Menggunakan SmartPLS (T. J. Santoso, C. M. Wibowo, & I. Yunianto, Eds.). Yayasan Prima Agus Teknik bekerjasama dengan Universitas Sains & Teknologi Komputer.

- Dwirandra, A. (2018). Pengaruh Independensi, Kompetensi, Integritas, dan Struktur Audit Terhadap Kualitas Audit Kantor Inspektorat AA Ngr Agung Wira Gita.

- Edison, Emron, Yohny, A., & Imas, K. (2016). Manajemen Sumber Daya Manusia. Alfabeta.

- Geiger, marshall, & Raghunandan, P. (2002). Auditor tenure and audit reporting failures. Auditing: A Journal of Practice & Theory, 21, 67–78.

- Ghozali, I. (2006). Aplikasi Analisis Multivariate Dengan Program SPSS. Badan Penerbit Universitas Diponegoro, Semarang, 4.

- Ghozali, I. (2018). Aplikasi Analisis Multivariate Dengan Program IBM SPSS 25. Badan Penerbit Universitas Diponerogo.

- Hadi, S. S., Murifal, B., & Revita, D. E. (2019). Auditing. Graha Ilmu.

- Hermawan, A., & Damayanti, D. Ri. (2018). Kualitas Audit dan Manajemen Laba (D. Achmad, Ed.; 1st ed.). Adhi Sarana Nusantara.

- Hermawan, S., Maulana, R., Adinda, K., Maulana, M. T., & Fauza, R. R. (2020). Buku Ajar Perlukah Rotasi dan Promosi Jabatan? (M. T. Maulana & R. R. Fauzan, Eds.). UMSIDA Press.

- Juliantari, N. W. A., & Rasmini, N. K. (2013). Auditor Switching dan Faktor Faktor yang Mempengaruhinya. E-Jurnal Akuntansi.

- Junaidi, Jogiyanto, H., Suwardi, E., Miharjo, S., & Hartadi, B. (2016). Does Auditor Rotation Increase Auditor Independence? Gadjah Mada International Journal Of Business, 18.

- Kalanjati, D. S., Nasution, D., Jonnergård, K., & Sutedjo, S. (2019). Auditor rotations and audit quality Auditor rotations and audit quality A perspective from a cumulative number of audit partner and audit firm rotations. Emerald Publishing Limited, 27, 1321–7348.

- Keputusan mentri agama No.1251 tahun 2021, Kementerian Agama Republik Indonesia.

- Nur Alimin Azis. (2021). Model_interaksi_independensi_auditor. Penerbit NEM.

- Nurdin, Ismail, & Hartati, S. (2019). Metodologi Penelitian Sosial. Surabaya: Media Sahabat Cendekia.

- Nurhasanah, S. (2023). Statistika Pendidikan: Teori, Aplikasi, dan Kasus (2nd ed.). Penerbit Salemba.

- Oziegbe, David, Odien, & Ruth. (2022). Auditors' Independence, Audit Tenureship, Firm Characteristics, and Audit Quality: Evidence from Nigeria. The Journal of Accounting and Management, 12.

- Pasaribu, B. (2021). Teori Pohon Kompetensi.

- Peraturan kepala badan pengawasan keuangan dan pembangunan No.PER-211/K/JF/2010.

- Peraturan kementerian pariwisata, Pedoman deputi bidang industri dan investasi No. PDM/1/11.00.00/D4/2023.

- Peraturan kementerian pariwisata No.18 tahun 2021, Kementerian pariwisata Republik Indonesia.

- Prabowo, D., & Suhartini, D. (2021). The effect of Independence and integrity on audit quality: Is there a moderating role for E-Audit? Journal of Economics, Business, and Accountancy Ventura, 23, 305–319.

- Putri, A. N., & Pohan, H. T. (2022). Pengaruh Audit Tenure, Rotasi Audit, dan Ukuran Perusahaan terhadap Kualitas Audit. Jurnal Ekonomi Trisakti, 2(2), 919–928.

- Rutherford, R. D. (1993). Statistical Models For Casual Analysis. Program on Population East-West Center, Honolulu, Hawai.

- Said, L., & Munandar, agus. (2018). The influence of auditor’s professional skepticism and competence on fraud detection: the role of time budget pressure. Jurnal Akuntansi Dan Keuangan Indonesia, 15(1), 6.

- Sangadah, L. (2022). Pengaruh Akuntabilitas Auditor, Independensi Auditor, Dan Profesionalisme Auditor Terhadap Kualitas Audit. Owner: Riset Dan Jurnal Akuntansi, 6, 1137–1143.

- Slamet, R., & Hatmawan, A. A. (2020). Metode Riset Penelitian Kuantitatif Penelitian Di bidang Manajemen, Teknik, Pendidikan Dan Eksperimen. Yogyakarta: Deepublish.

- Sofyan, Y., & Heri, K. (2009). SPSS Complete: Teknik Analisis Statistik terlengkap dengan software SPSS. Salemba Infotek.

- Sudrajat, L. A. and R. A. and P. E., Lalu, A., Rifai, Ahmad, Pituringsih, & Endar. (2019). Pengaruhtime budget pressure, kompleksitas audit, dan skeptisisme profesional auditor terhadap kualitas hasil pemeriksaan (studi empiris pada inspektorat se-pulau lombok. Jurnal Akuntansi Aktual, 3, 135–145.

- Sugiyono. (2018). Metode Penelitian Kombinasi (Mixed Methods). . Bandung: CV Alfabeta.

- Syofyan, E. (2022). Pengaruh Rotasi Audit, Tenura Audit dan Spesialisasi Auditor tehadap Kualitas Audit (Hayat, A. Sofiuddin, & A. Murtadlo, Eds.; 1st ed., Vol. 1). Unisma Press.

- Tjun, L., Marpaung, E. I., & Setiawan, S. (2012). Pengaruh Kompetensi dan Independensi Auditor Terhadap Kualitas Audit. Jurnal Akuntansi , 4.

- Undang undang No.13 Tahun 2003, tentang ketenagakerjaan, Negara Kesatuan Republik Indonesia.

- Vu, Doan Anh and Hung, & Nguyen Xuan. (2023). Factors Influencing the Auditor Independence and Affects to Audit Quality of the Supreme Audit Institution of Vietnam. International Journal of Professional Business Review, 8, 2197.